Capital Investment LLC UAE: Setup Basics for Property Deals

Capital Investment LLC UAE setup basics for property deals: choose mainland or free zone, plan compliance and banking, and execute off-plan purchases smoothly.

Buying property through a company is no longer just a “large investor” move in the UAE. In 2026, more international buyers are using a capital investment LLC UAE structure to ringfence liability, bring in partners, simplify succession, and keep deal execution clean across multiple acquisitions.

But the UAE has several company regimes (mainland, free zone, and other holding vehicles), and the “right” setup depends on what you are actually doing with the property: holding a single off-plan unit, building a rental portfolio, flipping on assignment, or mixing personal use with investment.

This guide covers the setup basics you should understand before you form an LLC for property deals, including the core decisions, compliance expectations, and how corporate ownership typically flows into a purchase.

What “LLC” means in the UAE (and why it’s used for property)

In simple terms, an LLC (limited liability company) is a company where owners’ liability is generally limited to their share capital, subject to legal and contractual exceptions. In the UAE, “LLC” commonly refers to a mainland limited liability company licensed by an emirate’s Department of Economy and Tourism (or equivalent licensing authority). Many free zone companies also offer limited liability, even if the legal label is not always “LLC” in the branding.

Investors use a company for UAE property deals to:

- Ringfence risk (tenancy claims, contractor issues, bank covenants, co-investor disputes).

- Bring in partners with clear shareholding and governance.

- Separate personal and investment assets (useful for multi-asset strategies).

- Streamline succession and continuity (especially for families or multi-generational planning).

- Create cleaner reporting for lenders, auditors, or a family office.

Important: a company structure does not automatically create tax-free outcomes in your home country. It can also add ongoing compliance and banking friction, especially for non-resident owners.

First decision: what is the company actually going to do?

Before you choose “mainland vs free zone”, define your real-world use case. The licence activity, banking profile, and even property eligibility can change based on this.

Common property-driven objectives include:

- Hold a single off-plan unit until handover, then rent or sell.

- Hold multiple units across emirates under one entity.

- Operate short-term rentals (this can introduce additional licensing requirements at the property level).

- Buy, refurbish, and resell (higher AML scrutiny, and you may need a licence activity aligned with trading or development related services).

- Owner-occupier purchase via company (possible in some cases, but can be inefficient and complicate personal visa and insurance arrangements).

If your plan includes collecting rent, signing leases, hiring contractors, or engaging a property manager, you should expect a bank to ask for a clearer operational story than “holding company”.

Mainland vs free zone: the practical difference for property deals

The UAE gives you multiple incorporation pathways. For property investors, the decision is usually driven by (1) where you need to do business, (2) bank account practicality, and (3) whether the developer or land department accepts the entity for registration.

Here is a high-level comparison.

| Setup route | Typical use for property investors | Main advantages | Common constraints to plan for |

|---|---|---|---|

| Mainland company (often called LLC) | Buying and holding property, leasing, contracting locally | Broad ability to contract in the UAE and interact with local counterparties | Office or premises requirements can apply, process can be more document-heavy |

| Free zone company | Holding assets, structuring for non-resident owners, consolidated investment vehicles | Often faster setup experience, strong support ecosystems in many zones | Doing business “onshore” may need extra steps depending on activity, some counterparties prefer mainland |

| Other holding vehicles (varies) | Specialist structuring, estate planning, multi-jurisdiction ownership | Can help with governance and succession | Eligibility for property registration can vary by emirate and by freehold zone, always verify acceptance before you buy |

There is no universal best answer. The key is to verify acceptance for the exact property transaction you intend to do before you incorporate, not after.

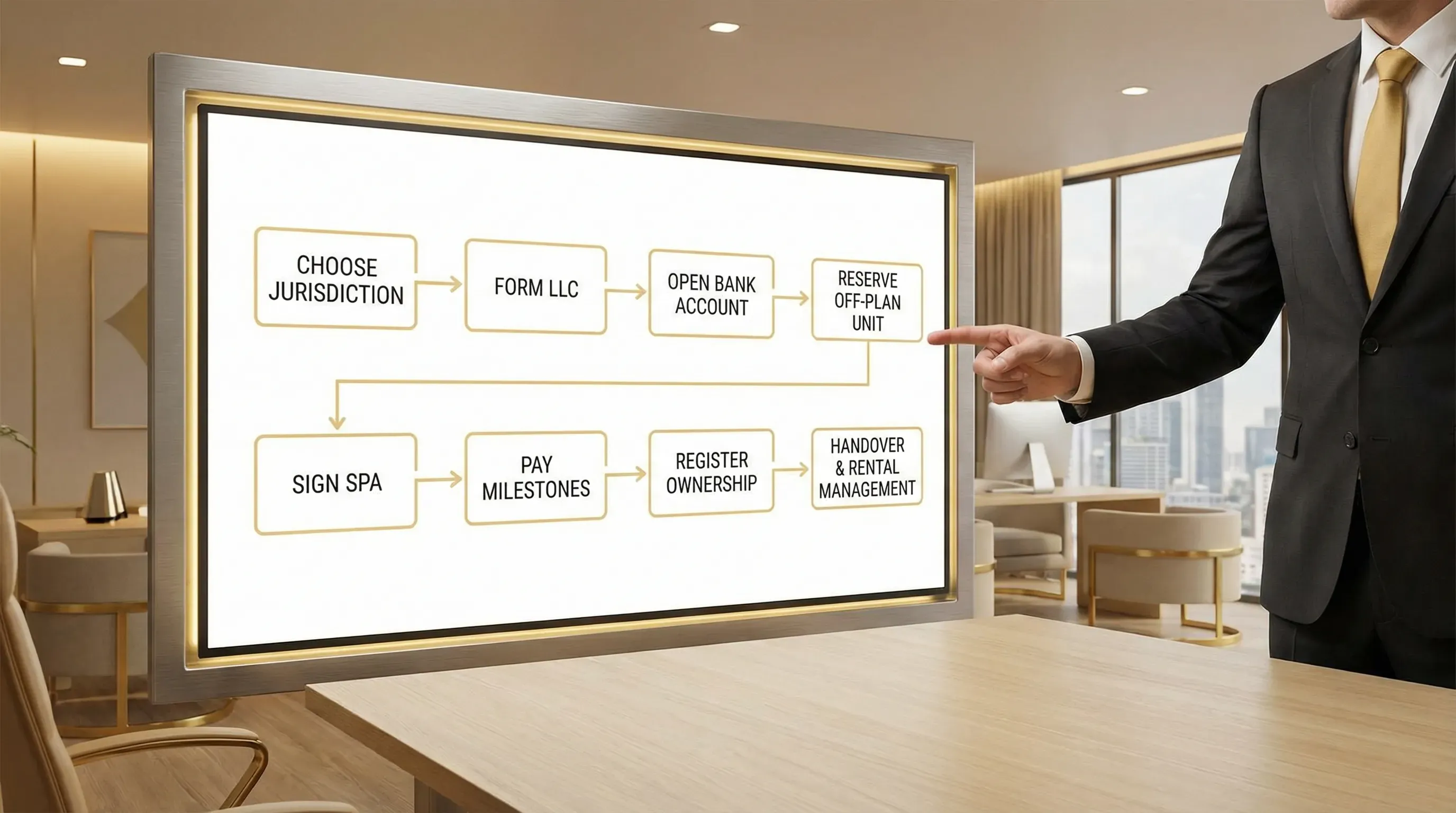

The “setup basics” checklist (what happens in most formations)

Company formation steps vary by authority, but most UAE setups for a property-focused LLC or limited liability company include the same building blocks.

1) Choose jurisdiction and licensing authority

Your jurisdiction will dictate the process, the compliance expectations, and sometimes how banks view the company’s risk profile.

Questions to answer:

- Will you sign contracts inside the UAE with developers, brokers, contractors, or tenants?

- Do you want a setup aligned with a specific emirate (for example, if your acquisition pipeline is mostly in Ras Al Khaimah)?

- Do you need physical office space, or can you use flexi-desk arrangements (where available and accepted)?

2) Define activity and shareholder structure

The activity on your trade licence matters because banks and counterparties use it to assess whether your transactions “make sense”. If you are forming a company for property holding and investment, you want activities that clearly align with that objective.

At this stage you also define:

- Shareholders (individuals, corporates, or a mix)

- Share percentages

- Authorised signatories (who can sign contracts and operate bank accounts)

3) Prepare governance documents (and make them usable for property purchases)

Most investors focus on incorporation speed and forget the property execution details.

Two practical points:

- Ensure the authority to buy and sell property is clearly covered in company documents and shareholder resolutions.

- If you will buy off-plan, make sure the company can sign a Sale and Purchase Agreement (SPA) and later handle handover tasks (utilities, snagging, insurance, leasing).

4) Plan for Ultimate Beneficial Owner (UBO) and AML expectations

UAE authorities and banks apply UBO and anti-money laundering checks. Even if your company is simple, expect questions about:

- Source of funds

- Source of wealth

- The real persons behind any corporate shareholders

- Transaction rationale (why this company, why this emirate, why this property)

The UAE Ministry of Economy maintains UBO-related compliance expectations and guidance. You can start at the official ministry portal for regulatory context: UAE Ministry of Economy.

5) Open a bank account (often the longest pole)

For many non-resident investors, bank account opening is harder than incorporation.

Practical realities in 2026:

- Timelines vary widely depending on shareholder profile, nationality, business activity, and documentation quality.

- Some banks prefer operating businesses over pure holding companies.

- You should expect enhanced due diligence if funds originate from multiple jurisdictions or if the structure has layers.

If your investment involves staged off-plan payments, align the bank account timeline with the payment schedule early, so you do not end up rushing transfers at unfavourable FX rates.

6) Understand ongoing compliance and tax registration triggers

Even a “simple” property holding company can have ongoing obligations.

Two key regimes to understand:

- UAE Corporate Tax (introduced for financial years starting on or after 1 June 2023). The headline rate is 9 percent on taxable income above AED 375,000 (with reliefs and special rules in some cases). Always confirm your position with a qualified tax adviser. Start with the official overview from the Federal Tax Authority (Corporate Tax).

- VAT. Many residential property transactions are VAT-exempt or zero-rated depending on the nature and timing of supply, but businesses can still have VAT obligations based on taxable supplies and thresholds. The standard VAT registration threshold is AED 375,000. See the Federal Tax Authority (VAT).

You do not need to become a tax expert to form an LLC, but you do need to design a structure that will not surprise you later.

How a company-owned property purchase typically works (ready vs off-plan)

Once the entity exists, the purchase process is broadly similar to buying personally, but corporate buyers should expect extra documentation steps.

Typical documents requested for a corporate buyer

Exact requirements vary by developer, broker, bank, and emirate, but corporate buyers are commonly asked for:

| Category | Examples of what is often requested | Why it matters |

|---|---|---|

| Company identity | Trade licence, certificate of incorporation, memorandum and articles | Confirms legal existence and permitted activity |

| Authority to sign | Board or shareholder resolution, POA if applicable, specimen signatures | Proves the signatory can bind the company |

| UBO and AML | UBO declaration, shareholder passports, corporate structure chart | Required for compliance and risk assessment |

| Banking and funds | Bank statements, source of funds explanation, remittance evidence | Supports AML checks and payment acceptance |

| Transaction specifics | Reservation form, SPA, escrow details (for off-plan), property unit details | Links the entity to the exact asset |

If you plan to buy remotely, ensure your signing arrangements are recognised in the UAE. Many investors use a properly notarised and legalised Power of Attorney, but the format and acceptance can differ by authority and by transaction.

Off-plan purchases: align structure with Oqood and milestone payments

For off-plan property, the company usually:

- Reserves the unit (often with a booking amount)

- Signs the SPA

- Makes staged payments (often linked to construction milestones)

- Completes registration steps required by the relevant authority

- Handles handover, snagging, and post-handover operational setup

Because off-plan timelines can run for years, you should design the company’s banking, signatory, and compliance setup to remain stable even if shareholders move countries or renew passports.

Ready property purchases: title transfer and operational setup

For ready properties, the corporate buyer often needs to coordinate:

- Title transfer registration (or equivalent)

- Utility accounts and service charge arrangements

- Insurance in the company name (where relevant)

- Lease registration and property management setup if renting

The administrative burden can be slightly higher than personal ownership, but it is usually manageable if your documents and signatory powers are prepared properly.

Common mistakes when setting up a capital investment LLC in the UAE for property

Forming the company before confirming property acceptance

Not every structure is accepted for every development or freehold zone. Before you pay for incorporation, confirm with the developer and the relevant registration authority what entity types are accepted.

Choosing an activity that complicates banking

If the licence activity does not align with property holding or investment, banks may treat incoming and outgoing payments as inconsistent with the stated business. That can lead to delays, freezes, or repeated compliance queries.

Underestimating KYC time (especially for non-residents)

Non-resident shareholders often face additional checks. Build time buffers into your purchase plan, particularly if you are targeting a pre-launch allocation with a short payment window.

Missing a clean “authority to transact” paper trail

Developers and land departments commonly request resolutions authorising the purchase. If your corporate documents are vague, you may have to amend them mid-deal, which is rarely fast.

Treating the structure as tax advice

A company can be a smart risk and governance tool, but it does not replace cross-border tax advice. Your home jurisdiction may still tax rental income, gains, distributions, or controlled foreign company outcomes.

When an LLC is usually worth it (and when it is not)

An LLC structure is often worth considering if:

- You are buying multiple properties and want consolidated ownership and reporting.

- You have co-investors and need formal governance.

- You are planning succession and want continuity.

- You want to ringfence operational risk from other personal or business assets.

It may be unnecessary (or inefficient) if:

- You are buying a single unit with no partners and no future pipeline.

- You want maximum simplicity for personal banking, utilities, and leasing.

- Your timeline is extremely tight and corporate KYC would jeopardise allocation.

Practical next steps (a clear way to move from “idea” to execution)

If you are considering a capital investment LLC UAE setup specifically for property deals, take these steps in order:

Confirm the deal model

Decide whether your first acquisition is off-plan or ready, whether it will be let long-term or short-term, and whether you will add assets within 12 to 24 months.

Validate acceptance before incorporation

Ask the developer (or your adviser) what entity types are accepted for registration for the specific project and emirate.

Build a compliance pack upfront

Prepare a clean file that includes passports, proof of address, CV or business profile, source of wealth narrative, and a simple structure chart. This usually reduces banking friction.

Coordinate company setup with property strategy

If you are investing in high-growth off-plan markets such as Ras Al Khaimah, it can help to work with a specialist who understands both the property pipeline and the transaction mechanics. Azimira focuses on curated off-plan opportunities and investor guidance in the UAE, with particular emphasis on Ras Al Khaimah. You can explore their investment approach here: Azimira real estate investment.

If you want to sanity-check whether a company purchase is the right move for a specific unit, timeline, and exit plan, you can also speak with the team via the main site: Azimira.

Final word

Setting up a company for UAE property can be a strong strategic move, but only when the structure matches your deal flow, your banking reality, and the exact registration rules of the emirate and development you are buying into.

Treat the LLC as part of your investment infrastructure. Done correctly, it supports faster future acquisitions, clearer governance, and better risk control. Done hastily, it can slow down the very deal you are trying to secure.

Related articles

First Time Investment Property: 9 Checks Before You Buy

Buying a first time investment property? Use these 9 checks to validate budget, developer, costs, rental demand and exit plan before you buy in the UAE.

Investment Plan in UAE: A Simple Framework for 2026

Investment plan in UAE for 2026: a simple framework to set goals, pick assets, model returns, manage risk, and execute UAE property deals confidently.

High Growth Potential: How to Spot UAE Property Early

High growth potential in UAE property: learn the early signals, data checks and red flags to spot winning off-plan opportunities before prices move.