Property Real Estate Investment: A Practical UAE Guide

Property real estate investment in the UAE, made practical. Learn how to choose emirates, model net yields, and do due diligence for 2026.

Buying property in the UAE can be straightforward, but “straightforward” is not the same as “simple”. The difference between a solid property real estate investment and an expensive lesson usually comes down to fundamentals: which emirate you choose, how you model returns (net, not headline), and whether you treat due diligence as a process rather than a checkbox.

This practical guide is designed for international buyers and investors who want clear, UAE-specific decision tools in 2026, especially if you are considering off-plan opportunities alongside ready properties.

What “property real estate investment” means in the UAE (and what it doesn’t)

In UAE terms, a property real estate investment is typically one of four plays:

- Capital growth: buying where demand and infrastructure are compounding, then exiting after appreciation.

- Income: targeting stable leasing demand (long-let or short-stay) and optimising net yield.

- Hybrid: combining staged off-plan payments (capital efficiency) with a plan to rent at handover.

- Lifestyle plus balance sheet: an owner-occupier purchase that still needs resale and rental logic.

What it is not: a guaranteed return. The UAE is a rules-based, maturing market, but performance is still driven by micro-location, building quality, developer execution, ongoing costs, and timing.

The UAE investment landscape in 2026: the practical realities

A few UAE realities shape almost every investment decision:

The tax context is attractive, but structuring matters

The UAE is widely known for no personal income tax, and the property environment is often described as “tax-efficient”. However, investors still face:

- Upfront fees (registration, trustee or admin fees depending on emirate)

- Ongoing service charges (material to net yield)

- Potential VAT on commercial property (residential rules differ)

- Home-country taxation (for many overseas investors, rental income and gains may be reportable at home)

If you are investing via a company, remember the UAE introduced federal corporate tax, and profitability plus ownership structure can affect outcomes. Treat tax as part of your underwriting, not an afterthought.

“UAE property” is not one market

Dubai is not Ras Al Khaimah, and Abu Dhabi is not Sharjah. Liquidity, tenant profiles, seasonal patterns, and entry pricing differ widely.

A useful way to think about emirates is: maturity vs growth potential vs execution risk.

| Emirate | Typical investor appeal | What to watch closely | Best suited to |

|---|---|---|---|

| Dubai | Global liquidity, depth of demand, broad product range | Higher entry pricing in prime areas, project-by-project dispersion | Investors prioritising resale liquidity and market depth |

| Abu Dhabi | Institutional feel, stable demand pockets | Submarket selection matters, supply cycles | Buyers seeking stability and long holds |

| Ras Al Khaimah | Emerging luxury and tourism-driven story, value entry points | Delivery timelines, micro-market depth, management quality | Growth-focused buyers, off-plan strategies, lifestyle-linked demand |

| Sharjah / Northern emirates (non-freehold areas vary) | Affordability and local demand where rules allow | Ownership rules and foreign eligibility, resale constraints | Buyers with specific use-cases and clear legal eligibility |

Before you shortlist properties, shortlist the market mechanics you are actually buying into.

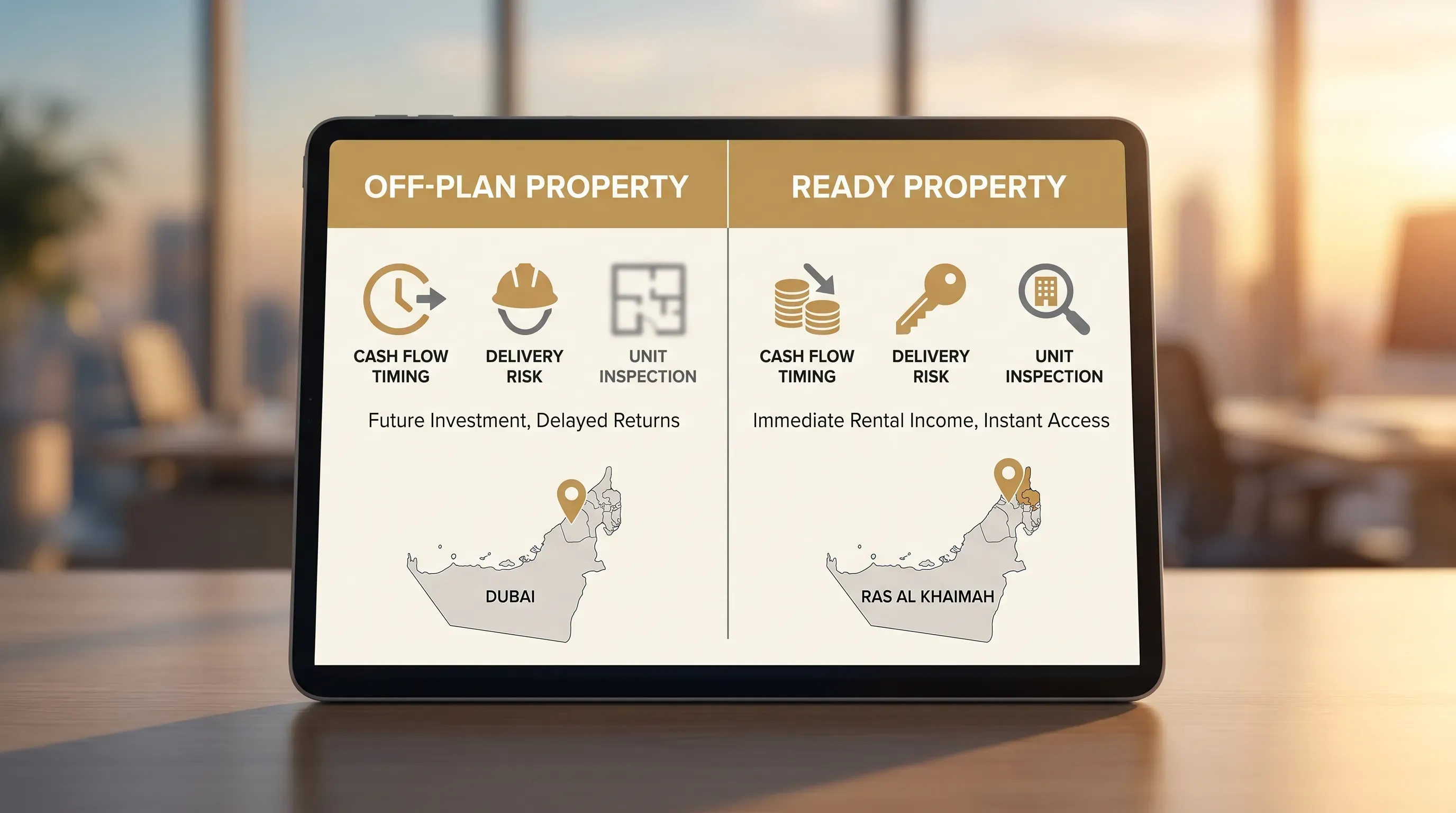

Off-plan vs ready property: a decision framework you can actually use

Many investors default to “off-plan equals higher ROI” or “ready equals safer”. Both are incomplete.

When off-plan can make sense

Off-plan can be compelling in the UAE because you may get:

- Staged payment plans (capital efficiency)

- Earlier entry pricing compared to near-completion stock

- Access to premium unit selection in early phases (views, stack, layout)

But you must underwrite two extra risks:

- Delivery risk (timelines, specification drift, community completion)

- Market risk at handover (rent levels and resale liquidity in that specific year)

When ready property can make sense

Ready property typically gives you:

- Immediate rental income (if tenant demand exists)

- A tangible asset you can inspect (build quality is less theoretical)

- Clearer net-yield modelling (service charges and utilities are known)

The trade-off is that you often deploy more capital earlier, and your upside may be more dependent on broader market appreciation.

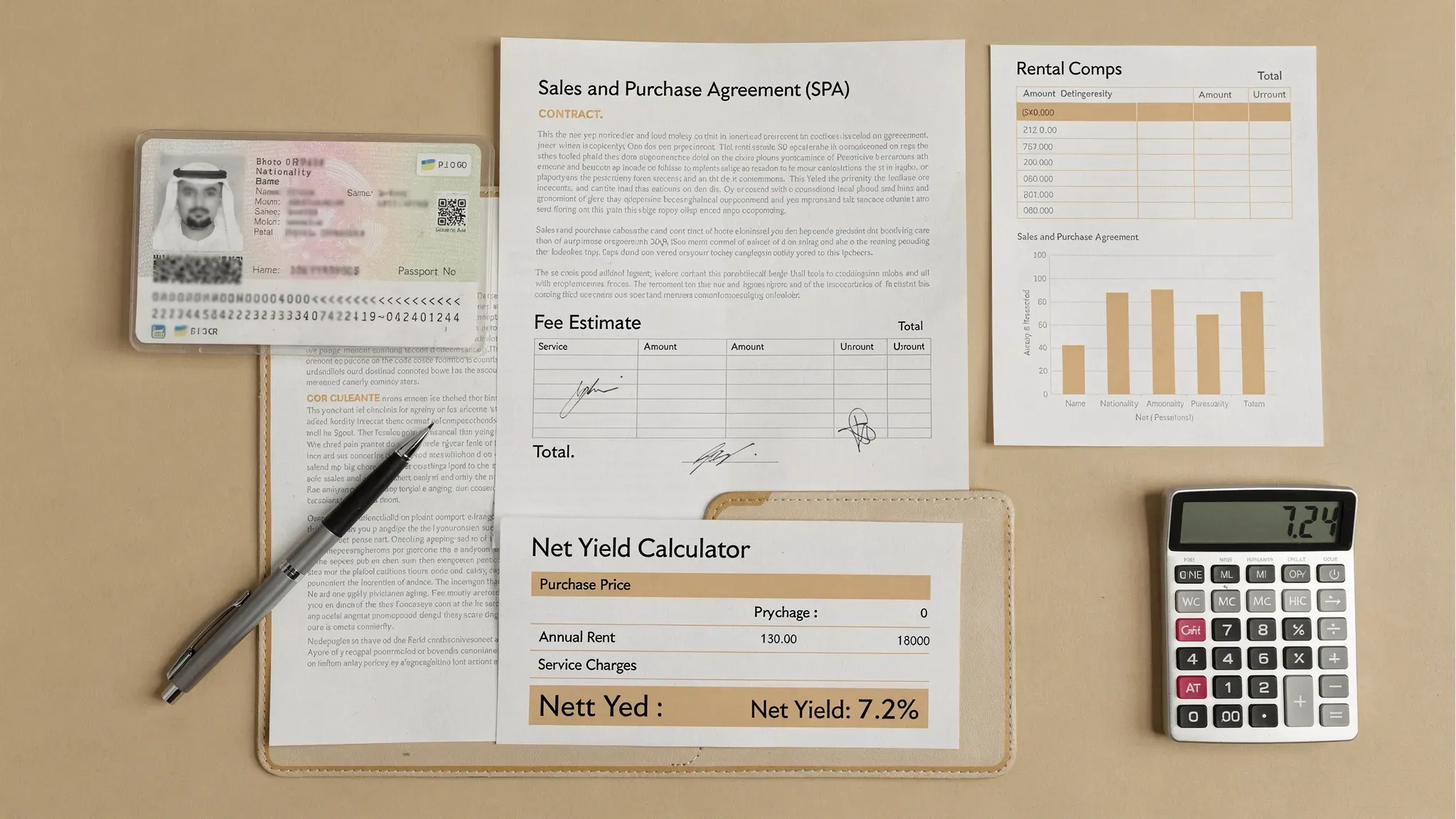

The underwriting basics: how to model returns without fooling yourself

If you only take one thing from this guide, make it this: headline yields are marketing, net yields are investing.

A simple net yield formula

Net yield is not complicated, but it must be consistent.

Net yield (%) = (Annual rent minus annual running costs) ÷ Total cash invested

Where “annual running costs” usually includes:

- Service charges

- Maintenance reserve (even for new units)

- Letting and management fees (especially for overseas owners)

- Insurance

- Vacancy allowance

And “total cash invested” includes:

- Deposit and instalments paid (for off-plan, this changes over time)

- Registration fees and admin fees

- Furnishing (if applicable)

- Any financing costs you are paying directly

Track two return timelines, not one

UAE investors often mix timelines accidentally:

- Pre-handover return logic (price appreciation, assignment rules, staged payments)

- Post-handover return logic (rentability, service charges, tenant profile, furnishing strategy)

Write two mini models. If the investment only works under one timeline, you have learned something important.

Due diligence in the UAE: what “good” looks like

Due diligence is not only legal. In the UAE, it is also operational.

1) Developer and project credibility

For off-plan, your biggest risk is not the market, it is execution.

Practical checks to run:

- Delivery history in the same emirate (not just marketing claims)

- Evidence of quality at handover in prior projects (snagging outcomes matter)

- Clarity on what is included in the specification (appliances, smart home, parking, beach access, etc.)

- Payment schedule triggers and what happens if milestones slip

2) Contract and registration pathway

Your paperwork should match the emirate’s process (ready vs off-plan) and should be reviewed by a qualified professional.

As a buyer, be especially clear on:

- Reservation terms and refundability

- The Sale and Purchase Agreement (SPA) clauses around delays, handover definition, and defects liability

- How registration is handled (and the fees and timing)

3) Community fundamentals, not just the unit

In the UAE, communities can be investment ecosystems.

Check:

- Access roads and transport links (today and planned)

- Retail, hospitality and lifestyle anchors that support rent premiums

- Pipeline supply in the immediate micro-area (too much near-identical stock compresses rent)

4) Operational plan for overseas ownership

If you do not live in the UAE, your investment performance will be heavily influenced by operations:

- Who handles leasing and tenant screening?

- Who approves maintenance and what is the spend threshold?

- How are service charges paid from abroad?

This is also where disciplined tooling helps. Some investors use CRM-style workflows and automation to track documents, payment milestones, and maintenance tasks. If you want inspiration on business-grade automation and AI workflows, explore these AI and IT solutions and adapt the approach to your property operations.

Financing and cash planning: the questions that prevent forced sales

Many UAE property issues are not “bad properties”, they are bad cash plans.

Ask these cash questions before you reserve

- If the payment plan accelerates, can you fund it without selling other assets at the wrong time?

- If handover is delayed, can you carry the holding costs and keep your plan intact?

- If you intend to mortgage later, what conditions must be true (valuation, income criteria, property eligibility)?

Developer plan vs bank mortgage

Developer plans can be attractive due to lower initial cash outlay and simplicity, while bank mortgages can offer earlier ownership structure clarity and potentially different flexibility. The correct answer depends on your residency status, income documentation, currency exposure, and whether your strategy is income-first or growth-first.

Residency linkage: when it belongs in your strategy

Many investors consider the UAE because property can be aligned with residency goals.

Two practical points:

- Residency requirements and thresholds can change, so always verify current rules before committing.

- If residency is a key objective (for you or your family), treat the property selection as a compliance asset as well as an investment asset. That means conservative documentation, clear valuation logic, and clean ownership records.

In practice, many investors focus on the AED 2 million property threshold commonly associated with the UAE Golden Visa property route, then design the investment to stand on its own merits (location, quality, exit options) rather than relying on the visa benefit alone.

A practical “UAE investment readiness” checklist

Use this as a quick self-audit before you start viewing units or attending launches.

| Area | You are ready when you can answer | Why it matters |

|---|---|---|

| Goal | Am I buying for income, growth, lifestyle, residency, or a blend? | Drives emirate, asset type, and hold period |

| Horizon | What is my minimum hold period, and what would make me exit earlier? | Prevents emotional selling |

| Budget | What is my all-in budget including fees, furnishing, and reserves? | Avoids return dilution |

| Returns | What is my net-yield target and my downside scenario? | Stops you chasing marketing numbers |

| Risk | What is the single biggest risk in this deal (delivery, rent depth, fees, liquidity)? | Focuses your due diligence |

| Operations | Who manages tenants, maintenance, and payments if I am overseas? | Protects real-world performance |

Frequently Asked Questions

Is property real estate investment in the UAE safe for foreign buyers? Safety depends on where you buy and how you execute. The UAE has established registration systems and off-plan protections, but investors should still verify ownership eligibility, contracts, and developer credibility in the chosen emirate.

Is off-plan property always better than ready property in the UAE? No. Off-plan can offer payment-plan advantages and early pricing, but it introduces delivery and handover-timing risk. Ready property can offer immediate rentability and clearer net-yield modelling, often with higher upfront capital deployment.

What costs do investors commonly forget in UAE property purchases? The most missed items are service charges, furnishing and replacement cycles, vacancy periods, management fees for overseas owners, and transaction fees at purchase and sale.

Do I need to live in the UAE to invest in property? No, many investors buy remotely. The key is setting up a reliable legal and operational process, including document handling, secure payments, leasing, and maintenance management.

How do I compare Dubai vs Ras Al Khaimah for investment? Compare them by market depth and liquidity (often stronger in Dubai) versus entry pricing and emerging growth drivers (often a key appeal in Ras Al Khaimah). Then validate at the micro-location and project level.

How Azimira can help you invest with clarity

If you want a property real estate investment strategy built around real underwriting, not hype, Azimira can help you evaluate and access premium UAE opportunities, with a strong focus on high-growth markets such as Ras Al Khaimah.

Explore Azimira’s approach to curated opportunities and investor guidance at azimira.com or start with the current investment overview at Azimira Real Estate Investment.

Related articles

Real Estate Portfolio Management for Smarter UAE Growth

Real estate portfolio management for UAE investors: set goals, track KPIs, diversify across off-plan and ready assets, and rebalance for smarter growth.

How to Read the Dubai Property Index Before You Invest

Learn how to read the Dubai property index, spot misleading signals, and compare price vs rent trends so you can invest with confidence in 2026.

High ROI Investments in the UAE: What Still Works in 2026

High ROI investments in the UAE in 2026: what still works, which strategies fail, and how to assess off-plan and rental returns with a clear framework.