Real Estate Capital: How Investors Structure Deals in the UAE

Real estate capital in the UAE explained: learn capital stacks, SPVs, mortgages and off-plan payment plans, plus risk controls to structure smarter deals.

If you are investing in UAE property, “finding a good unit” is only half the job. The other half is structuring your real estate capital so that your money arrives at the right time, carries the right level of risk, and can be recycled into the next deal without surprises.

In practice, UAE investors think in terms of a capital stack (who funds the purchase and on what terms), a legal wrapper (who owns the asset and how), and a timeline (when capital is deployed, registered, and eventually returned).

This guide breaks down the most common deal structures used in the UAE, especially for off-plan opportunities, and the questions sophisticated investors ask before wiring a dirham.

What “real estate capital” means in the UAE

Real estate capital is the money that funds acquisition, completion, and ongoing ownership of property. In the UAE, the concept matters even more because many investors buy off-plan (before handover) and because the market attracts a large share of international buyers.

Most deals combine some mix of:

- Equity: your cash deposit(s) and any additional cash paid during the build.

- Debt: a bank mortgage (usually on completed property, and sometimes on off-plan through specific programmes).

- Vendor or developer financing: instalment payment plans that behave like structured credit even if they are marketed as “0% interest”.

The core structuring goal is simple: match your capital to the risk period.

- Construction-stage risk tends to be higher, so many investors prefer smaller upfront equity and milestone payments.

- Stabilised, income-producing assets may justify mortgage leverage if the rental profile supports it.

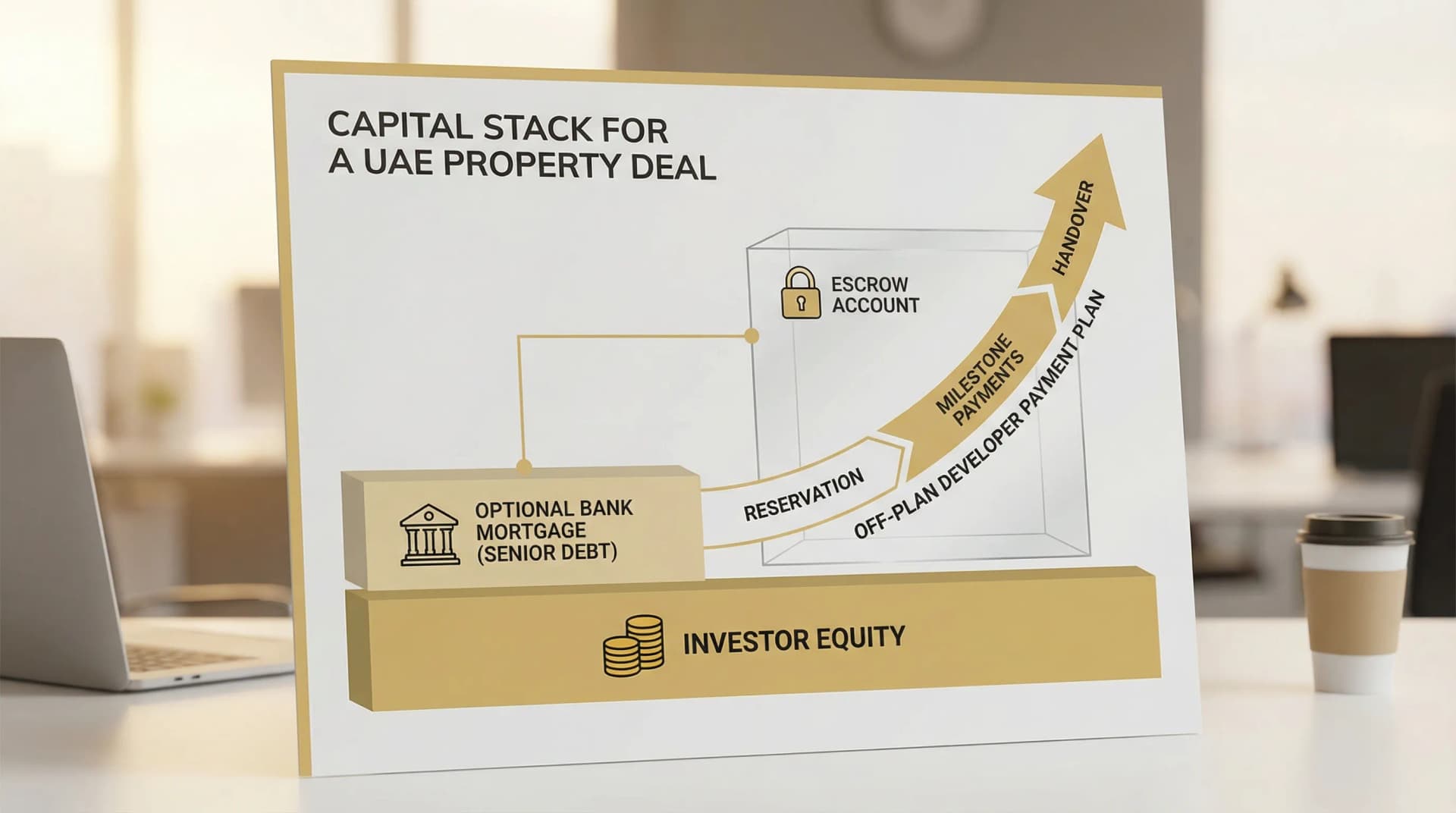

The three most common capital stacks investors use

While institutional investors can add layers like preferred equity and mezzanine debt, most private UAE property buyers use one of three structures.

1) All-cash (equity-only) purchase

This is the cleanest structure: no lender, no interest-rate risk, and typically the fewest moving parts at completion.

It can be especially attractive when:

- You are buying off-plan with a staged payment schedule.

- Your strategy is capital appreciation (rather than maximising cash-on-cash yield).

- You want speed and negotiating leverage, particularly at pre-launch.

The main trade-off is opportunity cost: equity tied up in one asset cannot be deployed elsewhere.

2) Mortgage + equity (classic leveraged buy)

A mortgage introduces a senior debt layer above your equity. In return, you may improve equity efficiency (more assets for the same cash). But leverage can reduce flexibility, especially if you plan to sell quickly or if rental cash flow is seasonal.

Mortgage structuring in the UAE is influenced by factors such as residency status, income source, property type, and lender appetite. For official banking and regulatory context, start with the Central Bank of the UAE.

3) Off-plan payment plan (developer financing effect)

Many off-plan purchases function like “capital calls” into a project. Your equity is deployed over time, typically through construction milestones.

Even though payment plans are not always framed as debt, they still create a financing profile you must manage:

- You have committed future payments that must be funded on schedule.

- Your “cost of capital” may show up as a higher purchase price, stricter assignment terms, or less pricing flexibility.

For the investor, the key question becomes: Can I fund every milestone comfortably under conservative FX and liquidity assumptions?

Quick comparison table: what changes by structure

| Structure | Where return typically comes from | What can go wrong | Best fit for |

|---|---|---|---|

| All-cash | Appreciation and/or rental income | Liquidity tied up, concentration risk | Investors prioritising simplicity and speed |

| Mortgage + equity | Rental yield plus leveraged appreciation | Rate changes, refinancing risk, approval timelines | Income-focused or portfolio builders |

| Off-plan payment plan | Pre-handover uplift and/or post-handover rental | Milestone stress, delays, resale restrictions | Growth-focused investors who can stage capital |

Ownership and “who holds the asset”: personal name vs SPV

Your capital stack answers “how it’s funded”. Your ownership structure answers “who owns it, controls it, and pays what”. In the UAE, common approaches include:

Personal ownership (in your own name)

This is the default for many buyers. It is usually operationally straightforward, but it may be less flexible for multi-investor governance, succession planning, or portfolio reporting.

Joint ownership (two or more individuals)

Often used by couples, family members, or partners pooling equity. The risk is rarely the property itself, it is the partnership.

If you structure this way, align early on:

- Who funds each instalment and what happens if someone cannot

- Who controls leasing, furnishing, and property management decisions

- What triggers a sale, and how disputes are resolved

SPV ownership (company holding)

An SPV can make sense for investors who want clearer governance, ring-fencing, or a scalable approach to holding multiple assets. The “right” SPV depends on investor nationality, tax profile, and how you plan to use the property.

Important: SPV structuring is legal and tax-sensitive, and the UAE has introduced corporate tax rules that can change outcomes depending on activity and revenue. Treat this as an advice-led decision (legal, tax, and compliance), not a template.

How off-plan deal structures actually work (capital timeline + legal controls)

Off-plan is where deal structuring and real estate capital planning really matter, because ownership rights and payment obligations evolve through stages.

A typical off-plan flow looks like this:

| Stage | Capital event | What investors should verify |

|---|---|---|

| Reservation | Booking fee or initial deposit | Agent/developer legitimacy, reservation terms, cancellation rules |

| SPA signing | Contract executed, larger deposit | SPA clauses (specs, delay remedies, default terms), fee schedule |

| Construction | Milestone instalments | Escrow mechanics, progress evidence, notice periods |

| Registration (off-plan) | Interim registration (varies by emirate) | Correct registration, receipts, reference numbers, authorised signatories |

| Handover | Final payment(s), snagging | Defects process, warranties, service charge clarity |

| Title issuance | Title deed (ready property) | Correct ownership details, mortgage registration if relevant |

Regulation is emirate-specific. Dubai is governed by the Dubai Land Department and its regulator RERA, while other emirates have their own land departments and procedures.

Escrow accounts: the capital protection mechanism you cannot ignore

For off-plan, escrow is designed to reduce the risk of funds being misused. From a structuring perspective, treat escrow as a non-negotiable control and confirm:

- Payments are made to the correct escrow account (not to personal accounts and not “outside the SPA”)

- Your receipts match the SPA buyer name and unit reference

- The agent or advisor can evidence the project’s regulatory status

If you want a deeper due diligence checklist, Azimira also covers this in The Essential Guide to Due Diligence for Off-Plan Property Escrow Accounts in the UAE.

Debt structuring: what experienced investors decide before they apply

A mortgage is not just “can I borrow”, it is “does leverage improve my risk-adjusted outcome”. In the UAE, experienced investors usually decide these points before shopping rates:

Fixed vs variable, and the holding period

If you expect to hold for a short to medium horizon, rate volatility matters more than headline rate. If you expect to hold long-term, refinancing and break costs may matter more than the initial deal.

Azimira’s Mortgage Rate Outlook: Comparing Fixed vs Variable Options in the UAE Property Market is a useful companion if you are weighing repayment stability against flexibility.

Cash-flow resilience, not just yield

A common mistake is modelling the deal on a single occupancy or rent assumption. Better underwriting asks:

- What happens if rent drops or vacancy extends?

- Can you still service the mortgage, service charges, and maintenance reserves?

- Do you have liquidity to cover handover-related costs (fit-out, furnishing, utilities, snagging)?

Exit friction: can you sell or refinance when you need to?

In real-world investing, the ability to exit is part of the capital stack. Liquidity, time-to-sell, developer NOCs, and bank release processes can all affect when your capital comes back.

Structuring returns: how investors think beyond headline ROI

Two investors can buy the same unit and achieve very different outcomes because of capital structuring.

Here is what tends to change performance in practice.

Deployed capital vs committed capital

Off-plan investors often commit to a total price, but only deploy part of it early. If the market rises during construction, returns on deployed equity can look very strong.

But that only holds if you can comfortably fund the remaining instalments. Your underwriting should reflect both:

- A conservative FX rate (for international buyers)

- A realistic buffer for delays or extended payment timelines

The “silent” costs that reshape IRR

IRR is highly sensitive to timing and friction costs. Common items that should be modelled upfront include:

- Land department registration and transfer fees (vary by emirate)

- Agency fees and mortgage-related fees (if applicable)

- Service charges and sinking fund exposure

- Letting, management, and maintenance costs

For a framework on return modelling (especially for UAE tax-efficient yield), see How to Project Your Real Estate ROI: A Comprehensive Guide to Calculating Tax-Efficient Yield in the UAE.

Governance and risk controls investors build into the deal

A strong structure is not only financial, it is procedural. Sophisticated investors commonly add controls that reduce the chance of a capital loss event.

Verification and documentation discipline

The most expensive problems in UAE property are often avoidable with simple checks. If you want an investor-friendly warning system, read 4 Red Flags That Scream Property Scam in the UAE.

In general, insist on:

- Clear buyer identity details on every document and receipt

- A complete SPA review (ideally by independent legal counsel)

- Proof of proper project registration and escrow details

Time-based risk management

Investors often align risk controls to the lifecycle:

- Pre-contract: developer due diligence, unit selection logic, downside scenarios

- During construction: progress monitoring, payment milestone tracking

- Pre-handover: snagging plan, warranty clarity, operational budget

- Post-handover: leasing strategy, property manager selection, insurance

Frequently Asked Questions

What is real estate capital in a UAE property deal? Real estate capital is the funding that supports the purchase and ownership of the property, typically a mix of investor equity, bank debt (mortgage), and off-plan payment plan commitments.

Is an off-plan payment plan considered debt? It is not always legally “debt”, but functionally it creates scheduled funding obligations similar to financing. Investors should treat it like a liability timeline and stress-test their ability to meet each milestone.

Should I buy UAE property in my personal name or via an SPV? It depends on governance, succession planning, tax, and compliance considerations. Many investors use personal ownership for simplicity, while portfolio investors may consider an SPV with professional legal and tax advice.

How do I reduce risk when wiring funds for an off-plan purchase? Use regulated channels, confirm the project escrow account details, ensure receipts match the SPA, and verify developer and agent credentials with the relevant land department or regulator.

Does a mortgage always improve returns in the UAE? Not always. Leverage can improve equity efficiency, but it can also increase downside risk through interest costs, approval timelines, and refinancing constraints. The right answer depends on your holding period and cash-flow resilience.

How Azimira helps investors deploy real estate capital more intelligently

Azimira connects investors and buyers with curated off-plan opportunities in the UAE, with a particular focus on high-growth markets such as Ras Al Khaimah. If you want to structure a deal that fits your risk tolerance and timeline, Azimira can support you with market insight, exclusive pre-launch access, and tailored investment strategy.

Explore Azimira at azimira.com or start with the investment overview at Investing in RAK Property to see how current opportunities are being positioned.

Related articles

What Counts as Good Real Estate Investments in 2026

Learn what makes good real estate investments in 2026, from net yield and demand signals to legal checks, exit plans and UAE opportunities.

Investors Needed for Real Estate? Start With This Plan

Investors needed for real estate? Use this practical plan to define strategy, numbers, due diligence and partners before raising capital.

Investment Marketing Tactics Developers Use at Launch

Understand investment marketing tactics developers use at launch, from scarcity to incentives, and learn how to assess UAE off-plan deals.