Properties and Real Estate in the UAE: A Buyer’s Quick Guide

Properties and real estate in the UAE explained fast: where to buy, off-plan vs ready, key fees, due diligence and next steps for buyers.

Buying property in the UAE can be refreshingly straightforward, but it is still a rules-driven market where the details matter. The fastest way to make a confident decision is to understand three things upfront: where foreigners can own, how the buying process works (especially for off-plan), and which costs and checks are non-negotiable.

This quick guide walks you through the essentials so you can compare options and move from browsing to reserving with clarity.

1) How UAE property buying works (the basics)

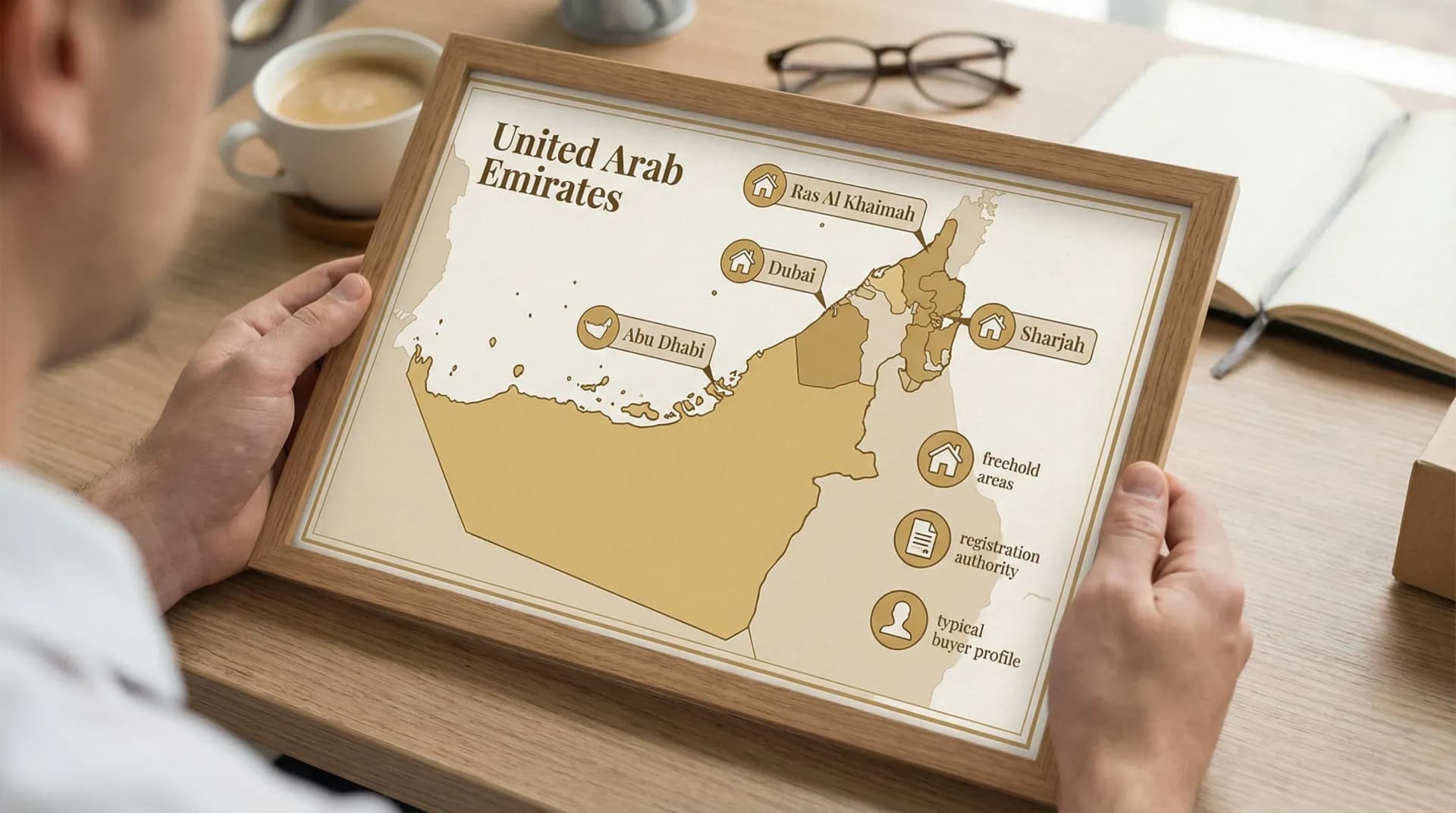

Freehold vs leasehold (and why location matters)

The UAE is not a single property market. Each emirate sets its own ownership rules, registration processes, and fees. For most international buyers, the key concept is freehold ownership in designated areas (often called investment zones). In practical terms, this means:

- You can own the property (and usually the unit’s share of common areas) outright.

- Ownership is recorded with the relevant emirate’s land department.

- Rules differ by location, property type, and sometimes by the specific master community.

Who regulates what?

A useful mental model is: federal laws set broad guardrails, emirate-level authorities run the day-to-day system.

Examples buyers commonly encounter:

- Dubai: Dubai Land Department (DLD) and the Real Estate Regulatory Agency (RERA).

- Abu Dhabi: Department of Municipalities and Transport (DMT) and associated platforms.

- Ras Al Khaimah: RAK Land Department and local real estate regulation for registration and services.

If you want the official starting point for residency pathways (including property-linked options), the UAE government portal on the Golden Visa is the best reference.

2) Define your “buyer type” before you choose a location

Two people can buy the same unit and get completely different outcomes. Your objective determines what you should prioritise.

Owner-occupier priorities

If you plan to live in the property, your shortlist should weight:

- Commute and connectivity

- School access and daily amenities

- Service charges and community management quality

- Floor plan usability and long-term liveability (not just a glossy brochure)

Investor priorities

If the goal is return on capital, prioritise:

- Demand drivers (employment hubs, tourism, infrastructure delivery)

- Rental strategy fit (long-let vs short-stay rules in that building/community)

- Developer track record (especially for off-plan)

- Exit liquidity (how easy it is to resell in that micro-market)

Azimira’s content library leans heavily into these investor questions, particularly for emerging growth markets like Ras Al Khaimah (for example, their broader investment overview).

3) Where to buy: a practical UAE shortlist

There is no universal “best emirate”, only the best fit for your budget, timeline, and risk comfort.

| Emirate | What it is known for | Best suited to | A quick watch-out |

|---|---|---|---|

| Dubai | Global liquidity, depth of inventory, strong end-user demand | Buyers who value market maturity and resale activity | Prices can move faster, and competition for prime units is high |

| Abu Dhabi | Institutional feel, stability, strong local fundamentals | Buyers who prefer a measured market and long-term positioning | Community-by-community dynamics vary, do not generalise |

| Ras Al Khaimah | Value and growth narrative, increasing premium development | Buyers targeting upside in an emerging luxury market | Due diligence on developer delivery and exact micro-location is critical |

| Sharjah | Strong resident demand and affordability in many segments | Resident-focused buyers (and some yield plays) | Foreign ownership rules and eligible zones require careful checking |

If you are comparing Dubai and Ras Al Khaimah specifically, you may also find Azimira’s market analysis pieces useful (for example, their data-led work on timing, yields, and community comparisons across RAK).

4) Off-plan vs ready property (fast decision framework)

A large share of UAE transactions involve off-plan (buying from a developer during construction). That can be a powerful wealth-building tool, but it is not automatically “better”.

| Question | Off-plan often fits when… | Ready often fits when… |

|---|---|---|

| Time horizon | You can hold through construction and want growth potential | You want immediate use or rental income |

| Cash flow | You prefer staged payments and flexibility | You prefer to pay once (cash or mortgage) and stabilise returns |

| Risk tolerance | You can manage delivery timing and specification risk | You want to reduce construction and handover uncertainty |

| Strategy | You want early-phase pricing or pre-launch positioning | You want a proven building, community, and rental comps |

If off-plan is on your radar, it is worth reading a deeper guide before you sign anything (Azimira’s practical guide to off-plan investing in the UAE is a solid next step).

5) The UAE buying process (from browsing to title deed)

Exact steps vary by emirate and by whether the property is off-plan or ready, but most purchases follow a similar flow.

- Set your buying criteria: budget, usage (live, rent, mixed), timeline, preferred areas, and any residency goal.

- Shortlist projects and verify eligibility: confirm the ownership type, freehold status (where relevant), and buyer eligibility for that zone.

- Reserve the unit: pay the reservation fee/deposit and ensure you receive written terms and the unit’s exact reference.

- Contract stage: for off-plan, this is the Sale and Purchase Agreement (SPA). For ready property, it may be an MoU and transfer file process.

- Due diligence and document verification: confirm developer status, escrow arrangements (for off-plan), unit details, and fee schedules.

- Financing (if applicable): mortgage pre-approval, valuation, and bank coordination. For off-plan, check lender appetite and stage payment rules.

- Transfer/registration: registration with the relevant authority and payment of applicable fees.

- Handover and post-purchase setup: snagging/inspection, utilities, insurance, and rental licensing if you will let the property.

For buyers focusing on Ras Al Khaimah, Azimira has a dedicated, practical reference on the authority side in their RAK Land Department guide.

6) Costs to budget for (the “don’t get surprised” list)

The UAE is often described as tax-advantaged for property owners, but buyers still need to budget for transaction and ownership costs. The mix changes by emirate and by building.

| Cost category | What it usually covers | Why it matters |

|---|---|---|

| Registration or transfer fees | Land department registration, transfer charges, admin | Can materially change your true break-even hold period |

| Agent fees | Brokerage commission (terms vary by market and deal) | Clarify who pays what, and what service is included |

| Mortgage fees (if used) | Arrangement fees, valuation, registration, insurance | Affects your cash-on-cash return, not just headline yield |

| Service charges | Building and community upkeep, shared facilities | High service charges can reduce net yield and resale appeal |

| Utilities and connections | Electricity, water, cooling (where applicable) | Impacts liveability and rental running costs |

| Maintenance and sinking fund planning | Repairs, wear-and-tear, replacements | Especially important for coastal properties and luxury finishes |

If you want a broader overview of the UAE’s tax position (and where fees still apply), Azimira also maintains a specific explainer on the UAE property tax landscape.

7) Due diligence that actually protects you

In a fast-moving market, the biggest mistakes are usually not about choosing the “wrong emirate”. They are about skipping verification steps that later become expensive.

What to verify before you commit

Use this as a practical checklist, and treat any resistance to basic verification as a red flag.

- Developer and project legitimacy: confirm the developer is properly registered for that emirate, and that the project is approved.

- Escrow and buyer protections (off-plan): understand how funds are handled and what triggers progress payments.

- Contract clarity: SPA clauses on handover date, specification, variation rights, penalties (if any), and termination conditions.

- Exact unit details: unit number, view orientation, floor plan version, parking, storage, and what is included.

- Community and building economics: service charges, facility scope, and any special levies.

- Rental rules: if you plan short-stay, confirm it is permitted in that building/community and what licensing applies.

If you are new to the region, it is also worth learning common scam patterns before you send money (Azimira’s guide on UAE property scam red flags is a quick read).

8) Financing and currency: the two silent deal-makers

Mortgages vs developer payment plans

UAE buyers commonly use either bank finance (mortgage) or developer payment plans (especially for off-plan). The right choice depends on your income profile, residency status, and risk tolerance.

If you are exploring bank finance, start with a comparison of requirements and realistic timelines (Azimira’s UAE mortgage comparison guide is designed for this).

International transfers (plan this early)

For many overseas buyers, the largest avoidable cost is not a fee, it is the exchange-rate spread and transfer friction. If you are buying off-plan with staged payments, you also need a currency plan for future instalments.

A simple rule: align your transfer strategy to your payment milestones, and ensure you can document source of funds for compliance.

9) Residency considerations (if it’s part of your plan)

Some buyers include residency as part of their decision. The UAE has multiple residency routes, and property can be one of them.

A widely referenced pathway is the 10-year Golden Visa, which (subject to current rules and eligibility) includes a property investment route often discussed around the AED 2 million threshold. Criteria and implementation details can change, so always verify against official guidance and get professional advice where needed.

Azimira publishes step-by-step, investor-oriented resources on this topic (for example, the Golden Visa application walkthrough).

How Azimira can help buyers move faster (without cutting corners)

A “quick guide” gets you oriented, but execution is where outcomes diverge. A specialist advisor is most valuable when they can shorten your path to the right unit and reduce avoidable risk.

Azimira focuses on connecting buyers and investors with curated off-plan projects in the UAE, with particular strength in high-growth markets like Ras Al Khaimah. If you want support with project selection, market insight, pre-launch access, and a strategy aligned to your goals, you can start here:

- Explore Azimira’s approach to real estate investment

- Or visit Azimira to enquire about current opportunities and tailored guidance

The goal is simple: help you buy the right property, in the right place, under the right terms, with a plan for what happens after completion.

Related articles

When to Buy Off Plan Property in the UAE

Learn when to buy off plan property in the UAE, from launch timing and market cycles to payment readiness, risk checks and 2026 buyer signals.

Real Estate Yield Explained for UAE Property Buyers

Real estate yield explained for UAE buyers: learn gross vs net yield, key costs, off-plan assumptions and how to compare returns.

Where Real Estate Investment Opportunities Are Shifting

Explore where real estate investment opportunities are shifting in 2026, from mature markets to UAE growth hubs like Ras Al Khaimah.