Property Sector Trends: What’s Shifting in the UAE for 2026

Property sector trends for 2026 in the UAE: shifting demand, supply discipline, RAK’s rise, sustainability, and rental strategy insights for investors.

The UAE property market is moving into a more selective phase for 2026. Demand remains deep, but buyers are more yield-aware, regulators are tightening standards around transparency and sustainability, and “where you buy” now matters as much as “what you buy”.

For investors, that’s good news, because a market that rewards fundamentals (connectivity, delivery track record, end-user depth, operating costs) tends to produce more predictable outcomes than one driven mainly by hype.

1) Macro conditions: from easy momentum to priced risk

Two macro forces are reshaping decision-making across the UAE property sector in 2026.

First, the cost of capital still matters, even in a region where cash buyers are common. Mortgage affordability influences end-user demand, and end-users influence resale liquidity. As the global rate cycle evolves, buyers are increasingly comparing developer payment plans, post-handover structures, and refinancing options as part of their total-return model.

Second, capital is more mobile and more sceptical. The UAE continues to attract international wealth, but that wealth is now better informed. Investors arrive with a shortlist, a spreadsheet, and a clear view of comparable opportunities across Dubai, Abu Dhabi, and emerging emirates.

The practical takeaway for 2026 is that projects with strong fundamentals can still outperform, but weaker launches will struggle to justify premiums.

2) Demand is shifting toward “liveable investment”

A key change is the continued blending of investor and owner-occupier preferences. Even when the buyer is purely investment-led, the tenant or future buyer is often an end-user with specific lifestyle expectations.

In 2026, demand is being pulled toward:

- Larger, more functional layouts (home office potential, storage, parking practicality)

- Community infrastructure (schools, healthcare access, retail, walkability)

- Mobility and commute logic (new transport links, road upgrades, airport access)

- Residency-aligned purchases, particularly where buyers are thinking about long-term optionality and family planning

This matters because it changes what “prime” means. A glossy brochure is not enough if a community lacks everyday liveability. Conversely, a less flashy location can outperform if it becomes a genuine residential hub.

3) Supply behaviour: developers are competing on structure, not just style

Across the UAE, the market has matured into one where payment terms and delivery confidence are part of the product.

In 2026 you will see more emphasis on:

- Staged releases and inventory discipline (developers pacing supply rather than flooding the market)

- More sophisticated payment plans that appeal to different buyer profiles (cash-flow focused vs capital growth focused)

- Clearer differentiation between developer tiers, with buyers paying closer attention to build quality, after-sales service, and handover track record

For off-plan investors, this is a positive shift. It means your due diligence can be anchored in more observable signals: escrow discipline, milestone alignment, specification clarity, and developer history.

If you want a regulatory baseline to start from, Azimira’s overview of UAE real estate regulations is a useful primer before comparing specific projects.

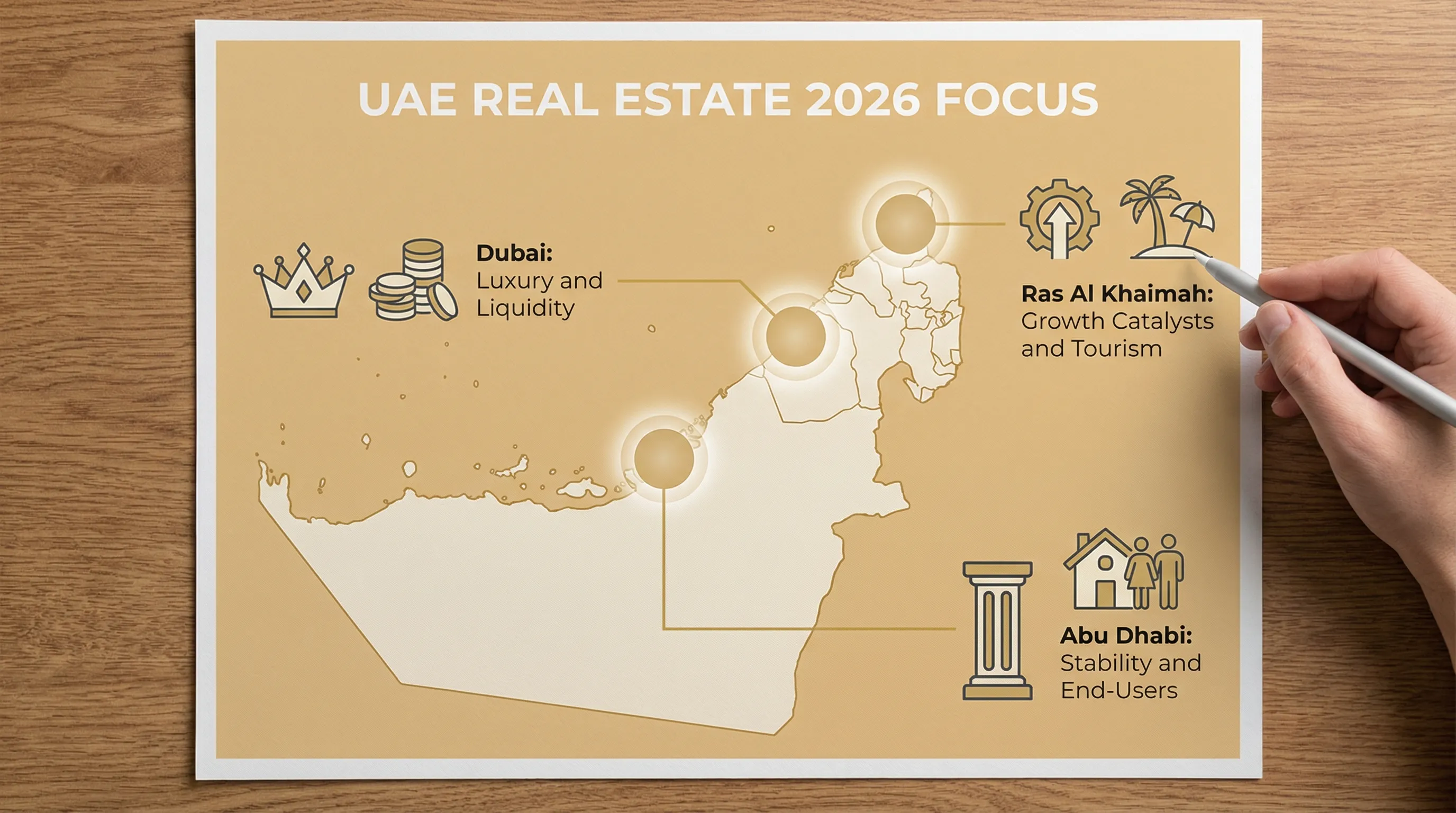

4) The UAE is becoming a multi-polar property market

Dubai still dominates global visibility, but the bigger 2026 trend is that performance is spreading across multiple emirates, each with a different role in a balanced portfolio.

Dubai: premium resilience, but buyers are more valuation-sensitive

Dubai’s strength remains liquidity, global demand, and depth across segments. What’s shifting is behaviour: buyers are less willing to overpay for generic “luxury”, and more willing to wait for the right unit, view protection, and developer.

Abu Dhabi: steady end-user depth and institution-led confidence

Abu Dhabi’s appeal is stability, stronger government and institutional footprint, and a growing premium lifestyle offering. In 2026 it continues to attract buyers who prefer a slower, more fundamentals-driven cycle.

Ras Al Khaimah: the emerging growth market with visible catalysts

Ras Al Khaimah (RAK) is the standout “new story” that has moved beyond speculation and into structured development. The investment case in 2026 is increasingly anchored to tangible catalysts: tourism build-out, infrastructure delivery, and global brand attention.

Azimira already covers RAK in depth across the site, so the key trend point here is simple: RAK is shifting from early-stage pricing to mid-stage pricing, which means entry strategy matters more than ever. Pre-launch access, developer selection, and unit-level scarcity (waterfront positioning, view corridors, proximity to anchor amenities) become decisive.

5) Sustainability is moving from “nice to have” to pricing power

Sustainability in the UAE property sector used to be mostly marketing language. For 2026, it is increasingly a cost and comfort equation that influences both rents and resale.

What’s behind the shift:

- Higher awareness of operating costs, especially cooling efficiency in a hot climate

- Tenant expectations rising in premium segments (air quality, insulation, efficient systems)

- Government direction, with the UAE’s long-term decarbonisation goals shaping building standards and investment flows (see the UAE’s Net Zero by 2050 strategic initiative)

For investors, the lens is practical: sustainability features should translate into either higher achievable rent, lower vacancy, lower maintenance burden, or stronger resale demand.

It’s also worth watching the global construction shift toward energy-efficient modular methods, which can improve delivery speed and predictability when done properly. While this is more visible in European housing, the underlying logic is relevant everywhere: controlled production, fewer site delays, and performance-led building standards. A good reference point for what that model looks like in practice is energy-efficient modular home building delivered on a fixed price and schedule.

6) Regulation and transparency are becoming competitive advantages

In 2026, the “trust layer” is a differentiator.

Across the UAE, buyers increasingly expect:

- Clearer documentation and cleaner transaction processes

- Better disclosure around service charges and community governance

- Stronger enforcement against misleading marketing

- More professionalised brokerage and advisory standards

This favours investors who operate with a repeatable process: verify the developer, verify the escrow arrangements, scrutinise the SPA, and model net returns rather than relying on headline yield.

7) The rental market is evolving into distinct strategies, not one blanket “yield”

Rental demand is not one market anymore. In 2026, performance is increasingly segmented by tenant type and lease length.

The most common strategies investors are comparing:

- Short-term rentals (STR) in tourism-led locations, which can offer higher top-line revenue but requires professional operations and regulatory compliance

- Mid-term corporate and project-based lets, often overlooked, but attractive where infrastructure and business activity create steady 3 to 9 month demand

- Long-let residential, which can look “less exciting” but often wins on risk-adjusted stability and lower operational intensity

The right strategy depends on your asset type, location, and your ability to manage variability. For example, a waterfront lifestyle unit may be STR-optimised, while a family community villa may perform better as a long-let with stable occupancy.

The 2026 trend map: what to watch, and why it matters

Here is a practical way to translate 2026 shifts into investor actions.

| 2026 shift in the property sector | What’s changing in the UAE | What it means for investors | What to check before you buy |

|---|---|---|---|

| Pricing power is more selective | Not every launch can command a premium | Unit-level quality and scarcity matter more | View protection, competing future supply, community completion timeline |

| Payment plans are part of the “return” | Developers compete on structure and flexibility | Cash-on-cash outcomes depend on staged payments | Milestone alignment, post-handover terms, fees and penalties |

| Sustainability affects rentability | Efficiency is becoming a tenant expectation | Better buildings can reduce vacancy and support pricing | Cooling efficiency, insulation quality, glazing, maintenance profile |

| Multi-emirate allocation is rising | Dubai is not the only growth story | Portfolio construction across cycles is easier | Liquidity, exit options, and local demand depth by emirate |

| STR vs long-let is a strategic choice | Rental markets are fragmenting | Different strategies require different assets | Licensing, management costs, realistic occupancy assumptions |

| Transparency is a competitive edge | Buyers are more documentation-led | Lower risk and smoother exits for clean assets | SPA clarity, escrow verification, service charges, handover record |

How to position yourself for 2026 without overcomplicating it

If you are planning a UAE purchase in 2026, you do not need to predict every macro variable. You do need a disciplined selection framework.

Start with a “three-layer” filter

Market layer: Choose an emirate and submarket supported by real drivers (connectivity, jobs, tourism, infrastructure).

Project layer: Evaluate the developer’s delivery track record, specification credibility, community plan, and governance.

Unit layer: Confirm scarcity, view protection, layout efficiency, and tenant fit.

Model returns the way the market now prices them

In a more mature market, net returns win. That means modelling:

- Service charges and maintenance expectations

- Vacancy assumptions aligned with your rental strategy

- Financing costs, if relevant

- Realistic rent ranges based on competing inventory

Use access as an advantage, not a shortcut

Exclusive or pre-launch access can be valuable, but only when paired with due diligence. The best outcome is not “getting in early” by itself, it is getting in early on the right project, with the right unit, on the right terms.

Where Azimira fits for 2026 buyers

Azimira focuses on premium off-plan opportunities in the UAE, with particular strength in high-growth markets such as Ras Al Khaimah. If your goal is to align a purchase with a clear investment strategy (capital growth, income, or a blend), the advantage of a specialist is not just sourcing, it’s helping you pressure-test assumptions: pricing, payment structure, liquidity, and risk.

If you are evaluating 2026 opportunities now, start by clarifying your target holding period and rental strategy, then build your shortlist around markets where the next 24 to 36 months of delivery and demand are most visible. That is where the UAE property sector is heading: less noise, more fundamentals, and more reward for informed buyers.

Related articles

Off the Market Real Estate: Pros, Cons, and Due Diligence

Learn how off the market real estate works, its pros and cons, and the due diligence checks that protect buyers in the UAE and beyond.

Property Market Analysis: The Data Signals to Track Monthly

Property market analysis made practical: track monthly price, volume, supply, rents and financing signals so you can time UAE deals with confidence.

Curated Portfolio: Build a Balanced UAE Property Mix

Curated Portfolio guide for a balanced UAE property mix. Learn how to combine growth, income, and diversification across emirates with clear rules.