Rental Property in the UAE: Yields, Costs, and Common Traps

Considering rental property in the UAE? Understand typical yields, true ownership costs, and common traps that cut returns, plus a practical checklist.

Most investors don’t lose money on a rental property in the UAE because the market is “bad”. They lose it because the deal they modelled on day one is not the deal they end up operating, once service charges, vacancies, furnishing, compliance, and management friction show up.

This guide is built to help you underwrite a UAE rental properly: what yields typically look like, which costs matter most, and the common traps that quietly cut returns in Dubai, Abu Dhabi, and high-growth markets like Ras Al Khaimah.

Gross yield vs net yield (the only number that matters)

You will see plenty of “8% to 10% yield” headlines in UAE property marketing. Treat those as a starting point, not an investment answer.

-

Gross yield is annual rent divided by purchase price.

-

Net yield is what is left after recurring costs and realistic vacancy assumptions.

In practice, two apartments with the same gross yield can deliver very different net yields depending on service charges, maintenance exposure, and how reliably the unit stays occupied.

If you want a deeper ROI modelling walkthrough (including cash-on-cash and tax-efficient structuring), Azimira’s ROI guide is a good companion: How to Project Your Real Estate ROI in the UAE.

Rental yields in the UAE: what “normal” looks like (and why it varies)

UAE yields are driven less by one “national average” and more by micro-markets: building quality, service charge levels, tourism demand (for short stays), tenant demographics, and new supply.

Broadly, investors tend to see:

-

Dubai: deep rental demand and liquidity, but pricing can compress yields in prime areas.

-

Abu Dhabi: steadier institutional demand in many pockets, often with a slightly different tenant mix.

-

Ras Al Khaimah (RAK): lower entry prices in many communities, with yield upside where tourism and infrastructure catalysts are accelerating demand.

Azimira’s own RAK market coverage frequently references mid to high single-digit long-term yields, with higher but more variable performance possible in well-positioned short-term rental assets. The important point is not the headline number, but what sits underneath it.

Typical yield ranges by strategy (use as a sanity check, not a promise)

| Strategy | What drives performance | What usually breaks the model |

|---|---|---|

| Long-term residential (12-month tenancy) | Tenant quality, rent index dynamics, unit efficiency, service charges | Underestimating vacancy, leasing fees, and maintenance; overestimating rent growth |

| Short-term rental (holiday home) | Seasonality, reviews, operator quality, furnishing and positioning | Low-occupancy months, licensing gaps, cleaning and maintenance churn |

| Hybrid (switch based on season) | Flexibility, pricing discipline, operational control | Operational complexity; regulations and building rules can limit flexibility |

If you are specifically considering RAK’s tourism-led upside, this analysis helps frame the demand split and what it means for yields: RAK Rental Demand Forecast: Tourism vs Resident Market Analysis.

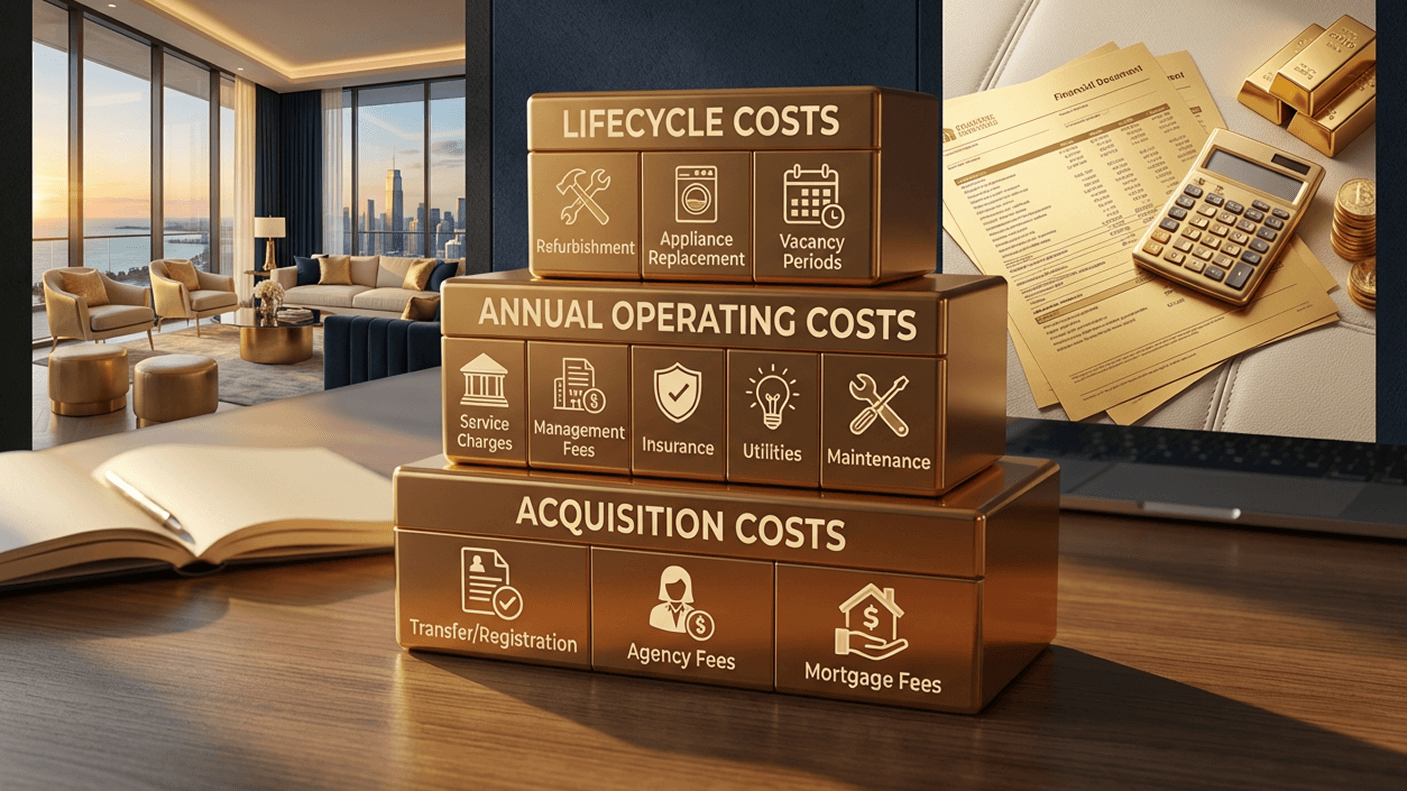

The real cost stack: what your rental property will actually pay for

To underwrite net yield, separate costs into:

-

Acquisition costs (one-off, at purchase)

-

Operating costs (recurring, every year)

-

Lifecycle costs (lumpy, every few years)

1) Acquisition costs (one-off)

These vary by emirate and deal structure, but typically include:

-

Transfer/registration fees charged by the relevant land authority.

-

Agency fees (if applicable).

-

Mortgage-related fees if financing (valuation, arrangement, life/property insurance depending on lender requirements).

-

Snagging and initial setup (especially if you buy off-plan or a unit that needs work before letting).

A useful example of how granular fees can be is Azimira’s breakdown for Ras Al Khaimah: RAK Land Department: Services, Fees, and Navigation.

2) Operating costs (recurring)

These are the costs that most often turn “great gross yield” into average net yield:

-

Service charges / community fees (often the biggest swing factor for apartments)

-

Property management fees (long-term or short-term, very different models)

-

Maintenance and call-outs (AC, plumbing, appliances, wear and tear)

-

Insurance (building is often covered by the master policy, but landlords usually still need contents/landlord cover)

-

Letting/renewal fees (market practice varies, and can be meaningful over time)

-

Vacancy allowance (even in strong markets, lease gaps happen)

3) Lifecycle costs (lumpy but inevitable)

Plan for replacements and refresh cycles, not just “repairs”:

-

AC servicing and occasional component replacement

-

Repainting between tenancies

-

Sofa, mattress, and appliance replacement (especially in short-term rentals)

-

Deep cleaning and consumables

A conservative model assumes these will happen even if the unit is new. New buildings often have defects and snagging issues too, just of a different kind.

Common traps that reduce UAE rental returns (and how to avoid them)

Below are the mistakes that show up repeatedly in real portfolios, including among experienced international investors.

Trap 1: Believing a brochure yield without pricing the expenses

Marketing yields are often calculated as:

(Annual rent) / (Purchase price)

That excludes service charges, vacancy, management fees, and maintenance. Net yield is where reality lives.

Fix: Model net yield with conservative assumptions and run a “bad year” scenario (lower occupancy, one major repair, slower tenant placement).

Trap 2: Underestimating service charges (or buying into a fee-heavy building)

In many UAE apartment investments, service charges are the swing cost. Pools, gyms, beachfront maintenance, concierge services, and premium common areas can be great for rentability, but they must earn their keep.

Fix: Ask for:

-

Current service charge schedule

-

History of increases

-

What is included (chiller, common area cooling, parking allocation, etc.)

If you are comparing two similar units, a materially higher service charge can erase the “better rent” advantage.

Trap 3: Modelling 100% occupancy (especially for short-term rentals)

Short-term rentals can outperform long-term yields, but they come with seasonality. RAK, for example, can be highly sensitive to holiday periods and event-driven demand.

Fix: Underwrite short-term rentals with:

-

A realistic occupancy range

-

Conservative average daily rate assumptions

-

A maintenance and replacement buffer

If you plan to operate remotely, operational excellence becomes part of your investment thesis. Azimira’s operational guide is a solid reference point: Remote-Manage Your RAK Airbnb in 7 Strategic Steps.

Trap 4: Ignoring the legal and compliance layer of letting

The rules and processes differ by emirate and rental type (long-term vs holiday home). Tenancy contracts, registration, notice periods, and lawful eviction rules matter because they shape your downside risk.

Fix: Understand the tenancy framework and use compliant contracts and processes from day one. For landlords focused on RAK, Azimira’s legal overview is a useful starting point: Tenant Rights in UAE: Essential Guide for RAK Landlords.

Trap 5: Treating off-plan “handover” as the same thing as “ready to rent”

Off-plan can be a smart way to target capital growth and secure better pricing, but the operational clock starts when you can actually rent the unit.

Common friction points:

-

Construction delays

-

Snagging and defect resolution timelines

-

Utility activation and building management handover

-

Finishing or furnishing gaps versus what tenants expect

Fix: Build a realistic post-handover runway in your plan (snagging, furnishing, photography, listing, tenant screening). Azimira’s rental income checklist gives a practical timeline view: The 6-Step Checklist to Getting Your First Rental Income from RAK.

Trap 6: Paying for “features” that tenants won’t pay for

Investors often overpay for what they personally like, rather than what the tenant segment values.

Examples that can go either way depending on micro-market:

-

Sea view premiums

-

Floor level (ground vs high)

-

Unit size mix (studio vs 2-bed)

Fix: Align the unit with the target tenant and leasing strategy, then price the premium against net yield. These Azimira analyses can help if you are weighing trade-offs:

Trap 7: Currency and cross-border cashflow blind spots

For overseas investors, “yield” can be diluted by FX spreads, transfer fees, and timing issues, especially with staged off-plan payment plans.

Fix: Treat money movement as part of the deal, not an afterthought. If your funding is international, build a transfer plan early (and consider rate-lock tools where appropriate). Example: Transferring SGD to UAE for Property: Banks, Fees, and Timing Guide.

Trap 8: Assuming “no tax” means “no structuring considerations”

The UAE is widely known for its favourable personal tax environment for many investors, but real estate still intersects with VAT in specific cases, corporate ownership decisions, and home-country tax rules.

Fix: Decide early whether you are buying personally or via a structure, and get cross-border advice if you are a non-resident. For RAK-specific pointers, see: The 5-Minute Tax Planning Guide for RAK Property Owners.

A practical net-yield “sanity check” (simple model)

You do not need a complicated spreadsheet to avoid most mistakes. You need a disciplined way to stress test the costs that actually move.

Here is a straightforward way to do it:

-

Start with expected annual rent (or expected annual revenue for short-term).

-

Deduct a vacancy allowance.

-

Deduct service charges.

-

Deduct management, maintenance, insurance, and letting/renewal costs.

A clean way to think about it is as an income statement for a single unit.

| Line item | What to include | Why it matters |

|---|---|---|

| Gross rent / revenue | Market rent or realistic STR revenue | Anchors the model in what tenants will pay, not what you hope |

| Vacancy allowance | Lease gaps, low-season occupancy | The most common “silent” return killer |

| Service charges | Building/community fees | Often fixed and unavoidable, regardless of occupancy |

| Management | Long-term PM or holiday home operator fees | You are buying an operating system, not just a unit |

| Maintenance & replacements | Repairs, AC servicing, appliance replacement buffer | Prevents one bad repair from wiping out a year’s profit |

| Insurance | Landlord/contents, liability where applicable | Protects the asset and reduces catastrophic downside |

| Letting & admin | Leasing commission, contract admin, marketing | More frequent in high-turnover strategies |

Once you have a conservative net income estimate, you can compare properties properly, including between emirates.

Due diligence checklist: what to verify before you buy a UAE rental property

Use this as a pre-purchase filter. It is intentionally practical.

-

Rental strategy fit: Is the building compatible with your intended letting model (long-term vs holiday home)?

-

All-in cost clarity: Do you have a written estimate of acquisition fees, service charges, and management costs?

-

Developer and project quality (off-plan): Track record, escrow compliance, and realistic handover runway.

-

Service charge risk: Current schedule, history, what is included, and whether amenities justify the cost.

-

Tenant demand reality: Who rents here, why, and what competing supply is coming nearby?

-

Operational plan: Who handles tenant screening, maintenance, inspections, and rent collection (especially if you live abroad)?

-

Legal process: Contract registration, notice requirements, and a clear dispute pathway.

-

Exit strategy: How liquid is the asset, and who is the next buyer (investor, owner-occupier, holiday-home buyer)?

If you want a fraud-prevention lens alongside the above, this is worth reading before you wire any money: 4 Red Flags That Scream Property Scam in the UAE.

Where Azimira fits (if you want a higher-conviction rental purchase)

If your goal is to buy a rental property in the UAE that performs on net yield (not just on paper), the advantage usually comes from better entry points and cleaner underwriting:

-

Access to curated off-plan projects and premium opportunities

-

Market insight that focuses on costs, demand depth, and realistic yield outcomes

-

Potential pre-launch access where pricing and incentives can materially improve returns

-

Tailored investment strategies based on your time horizon, risk tolerance, and whether you want long-term, short-term, or a hybrid approach

You can explore Azimira’s approach and request guidance at Azimira.

Related articles

What Counts as Good Real Estate Investments in 2026

Learn what makes good real estate investments in 2026, from net yield and demand signals to legal checks, exit plans and UAE opportunities.

Investors Needed for Real Estate? Start With This Plan

Investors needed for real estate? Use this practical plan to define strategy, numbers, due diligence and partners before raising capital.

Investment Marketing Tactics Developers Use at Launch

Understand investment marketing tactics developers use at launch, from scarcity to incentives, and learn how to assess UAE off-plan deals.